Are you already planning your retirement? It’s never too early to start thinking about it. You are probably saving in an employee pension plan or a registered retirement savings plan (RRSP).

Many Canadians worry about the sums they set aside. Are you saving enough to have a comfortable retirement? If you’ve already started considering where to find a free instant credit score, the answer is probably no.

How much you need to allocate toward these savings depends on your lifestyle, what retirement means to you, and what expenses you may have. Here are some thoughts to take into account.

When Should You Start Saving for Retirement?

It’s better to start saving for your golden years while you are still young and active. We advise you to set aside a certain percentage of funds from each paycheck. When you start saving later, you will need to increase the percentage of monthly income you need to set aside.

To avoid losing your years of compounding, you should begin this process earlier. The longer you set aside your money, the more funds you will eventually have for a comfortable retirement.

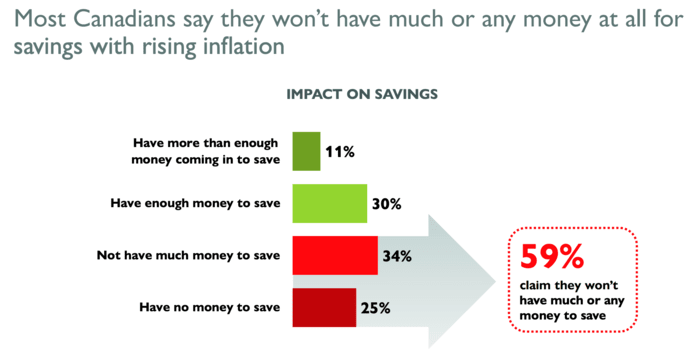

According to a Canadian Retirement study, 59 percent of Canadians claim they won’t have much or any money at all for savings. Only 30 percent of respondents stated they had enough funds to set aside in their savings accounts.

Another question to ask yourself is when you wish to retire. Do you want it to happen when you are 60 or 65? Some people prefer to keep on working part-time even after they turn 65, provided that they feel healthy and active. If you decide to retire earlier, you will also need to start saving earlier not to lose several contribution years.

Take Stock of Your Finances

The financial aspect is the most significant. It is the first thing that comes to your mind when you think about retirement planning. Will you have enough time to repay all your existing debt? Will you be able to save enough for a comfortable retirement? You have to take stock of your finances, and here are three retirement income streams:

-

Personal Savings Accounts

Do you have TSFA or RRSP to which you have been making contributions? These are the common types of accounts to save for retirement. If you follow smart strategies, you will be able to maximize your contributions and investments.

Understanding what savings will contribute to retirement will be useful in figuring out when you should take the plunge. Some consumers even realize they eventually have more funds than they thought.

-

Workplace Benefits or Pensions

Canadians who reach retirement age may have a pension available to them. Are you planning for retirement at the moment? Then you should consider different types of pension plans.

Should you open a Locked-in retirement account, a Defined Benefit Pension Plan, or a Defined Contributions Pension Plan? When you opt for a certain account, it will be easier to plan your income and have enough time to save for your retirement.

-

Government Benefits

Apart from the mentioned options, you may turn to government income opportunities. You should check if you qualify for a Guaranteed Income Supplement, Old Age Security, or Canada Pension Plan (or the Quebec Pension Plan).

There are particular implications and rules depending on when you want to begin accessing the funds and retire. You can also hire a professional advisor to guide you through this process and help you work towards reaching this target in terms of finances.

How Do You View Your Retirement?

Do you have a family and children? You need to consider how your retirement may influence them. Make sure you discuss the following aspects with your partner or spouse:

- Plans to retire with your spouse or partner. Whether your spouse is younger or older, you need to talk about your plans in case you desire to retire together. Retiring together with your partner requires particular considerations. You should talk about this option and think if it’s really possible. Working out a plan to set aside enough funds for your comfortable retirement will help you remain financially afloat and strive for your shared golden years together.

- Budgeting for a comfortable retirement. The second consideration is to budget for your retirement. Some people don’t want to change their lifestyle and dream of traveling overseas once they stop working. Others can’t save so much money and think about a quieter time when they quit work. Would you like to spend these years closer to your grandchildren and family? You should take some time to view these years in your head and imagine what type of lifestyle you want to have. Budgeting should be done according to your needs and wishes. Make a retirement budget no matter when you are planning to retire. Besides, consider inflation and the monthly and yearly costs of living in the future.

Review Your Retirement Savings Plan

Furthermore, we recommend you review your retirement savings plan once in a while. You can’t open the account and forget about it until your retirement. Talk to a financial advisor and review this plan at least once, even a couple of years.

Besides, when a major life event occurs (a divorce, the birth of a child, or the loss of a partner), you also need to check on your retirement savings plan and make possible changes if necessary. Negotiating these options with your financial planner or advisor is always a great idea. You will get professional assistance and possibly prevent mistakes.

The Bottom Line

It’s never too early to think about retirement. You may still be in your twenties or thirties now, but time goes by quickly. Depending on the age you wish to retire, you may need to start investing as early as possible.

While some people want to retire when they reach 60, others may continue working even when they are 65 or 70. The earlier you want to retire, the earlier you need to start saving and allocate a larger percentage of your paycheck to your retirement contributions.