Chargebacks are a multi-billion dollar threat to businesses and without proactive risk reduction and dispute management, retailers big and small could find themselves in financial duress. It’s vital to understand how the chargeback process works so you can prevent them and also successfully win disputes when needed.

That’s why we’re going to take a deep dive into the chargeback process. But first, let’s take a look at what chargebacks are.

-

Chargebacks Explained and What Merchants Must Know

A chargeback is essentially a forced refund issued by a bank to their cardholder(s). With chargebacks, the bank can claw back money already sent to a business and then return it to their customer’s account. Unlike traditional refunds, the customer is usually under no obligation to return the products or services rendered.

If a business gets hit with too many chargebacks, it may be designated high-risk and payment processors could increase the fees they charge. Companies will also have to pay chargeback fees (even if they win a chargeback dispute) and if they suffer too many chargebacks, these fees will rise.

In the United States, chargebacks were enshrined into law by Congress. Other countries too have established cardholders’ rights. The process outlined below covers chargebacks in the United States. While the process is similar in many other countries, you’ll want to do your homework and study the process in each country you serve.

With that said, let’s take a close look at how the chargeback dispute process works.

-

Cardholders Typically Start the Chargeback Process

Generally speaking, customers start the chargeback dispute by contacting their bank. Most banks offer clients a variety of ways to get in touch and start the process. Often, filing chargebacks is quite easy, and as a result, many people will quickly turn to their bank rather than the merchant.

The cardholder will explain their side of the story to the bank. A client could file a chargeback for a number of reasons, including:

- The product received was not as described.

- The retailer either didn’t offer a return policy or the process was too cumbersome to deal with.

- The goods arrived damaged, or never arrived at all.

- A thief stole and used the cardholder’s information to make an illegitimate purchase.

- The cardholder wants to use “friendly fraud” to score free stuff.

The last reason, “friendly fraud,” is especially common and many estimate that it makes up the majority of chargebacks. With friendly fraud, the cardholder will purchase something, say a tablet. When the tablet arrives, the customer will claim that they never received it, or that it arrived broken, or whatever else.

If the bank buys their story, they will file the chargeback. Ultimately, the card issuing bank approves or denies the chargeback, and they tend to side with the customer. And if the issuing bank does so, the fraudster will not only get his or her money back, but can also keep the tablet.

Meanwhile, the retailer losses the revenue from the sale, along with the product. The merchant must pay chargeback fees, and their chargeback ratio will rise.

During this initial phase, you can often prevent chargebacks by providing shipment tracking data, requiring signed delivery receipts, and by using dispute management platforms and other tools.

-

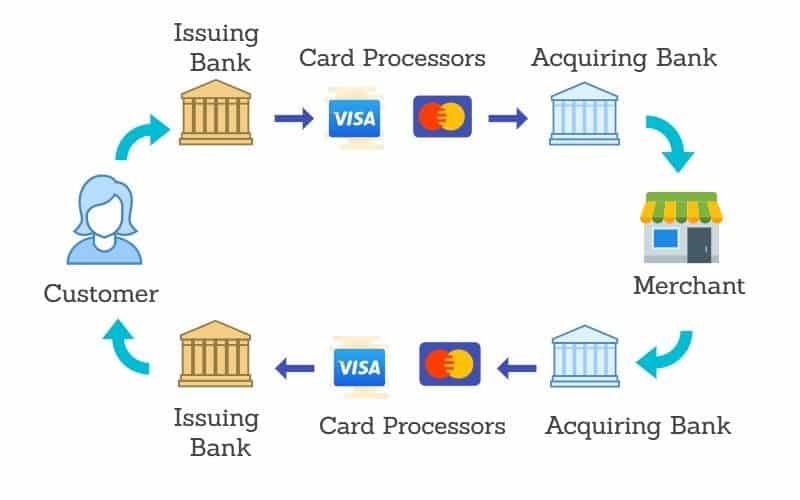

The Issuing and Receiving Banks Process the Chargeback

If the card-issuing bank sides with their client and files the chargeback, they’ll notify the receiving bank, which handles transactions on behalf of the merchant. The card issuer will then pass on the chargeback to the business. A reason code should be supplied. You should look this code up to understand why the chargeback is being filed.

Crucially, if you use a chargeback alert service, the issuing bank can warn the retailer before the chargeback is officially filed. This affords companies a chance to prevent the chargeback by offering a refund or taking other steps. If you succeed, you’ll deflect the chargeback.

If the dispute is not successfully deflected, the merchant can either accept or decline the chargeback. If you accept, you’ll have to refund the disputed amount. You’ll also have to pay chargeback fees and your chargeback ratio will rise. Most likely, you’ll lose the product or services rendered.

-

The Merchant Puts Together a Rebuttal Letter

If you accept the chargeback, the process concludes and the customer is refunded their money. However, if you decide to dispute the chargeback, you’ll have to put together a rebuttal letter. In this document, you’ll outline a case for why the purchase was legitimate, argue that you upheld your obligations, and request that the case be dismissed.

You’ll want to gather as much evidence as possible proving that the transaction was legitimate. Common and effective proof includes:

- IP addresses

- Communication with the customer

- Signed shipping receipts

- Card Verification Values (CVV)

Evidence in hand, you’ll write out your argument. It’s best to keep the letter short and to the point. During this phase, merchants must track deadlines to submit evidence and whatever else. If a deadline is missed, you may not be able to submit the evidence, thus hurting your case.

-

The Card Issuing Bank Approves or Rejects the Chargeback

The card issuing bank will then weigh the evidence and rebuttal letter against the customer and their claims. While banks are incentivized to side with their customer, a strong argument could sway the case in the merchant’s favor.

If the retailer wins, they’ll be given the funds in dispute. There is an important caveat, however: even if the business succeeds, it’ll still be on the hook for chargeback fees and its chargeback ratio will rise.

-

Second Chargebacks and Arbitration

Both cardholders and merchants may dispute the result of the first chargeback process. First, all parties involved will go through the whole process again. This is sometimes referred to as a “second chargeback.” And this phase itself is often called “pre-arbitration.” The outcome of the do-over typically only changes if new evidence is uncovered.

If the dispute still isn’t resolved after going through the second chargeback, the next step is arbitration. Either the merchant or customer can ask the Card Network (e.g. Visa) to step in as a neutral arbiter. Whoever losses arbitration will be on the hook for additional fees, which could be very expensive.

-

Managing Chargebacks and Disputes is a Hassle but the Right Tools Help

Understanding the chargeback process is vital for preventing and winning disputes. Without a proactive approach, companies could get swamped with chargebacks, and eventually, they may have to pay higher chargebacks and processing fees.

Managing disputes can be quite a pain, and if you miss important deadlines, the risk of losing the case greatly increases. Gathering evidence and putting together a rebuttal letter, in particular, is time-consuming. Fortunately, you can work with dispute management companies like ChargebackHelp, which furnish tools for preventing and fighting chargebacks.

These platforms often offer services for both managing current disputes and mitigating future issues. They also ensure that time is put to good use and will reduce burdens on businesses big and small. This way, organizations can focus on other vital business processes, like building inventory and marketing.